Knight Frank cautiously upbeat on Bangkok office situation

Knight Frank cautiously upbeat on Bangkok office situation

The first half of 2019 has seen Bangkok office rents soar to unprecedented levels, and while occupancy rates remain high, the influx of new supply over the next six months coupled with economic headwinds will be a real test for the market, as executive at Knight Frank Thailand said on Tuesday.

Executive director Marcus Burtenshaw also warned that tenants whose leases are expiring will face the problem of rising accommodation costs for the foreseeable future.

He said political uncertainty coupled with the US-China trade war has had a dampening effect on the Thai economy. The World Bank believes economic growth will fall to 3.5 per cent this year from 4.1 per cent the previous year.

Exports also contracted by 4 per cent in the first quarter 2019 – the first quarterly decline in three years – as the baht continues to appreciate against the US dollar.

Meanwhile, public investments in infrastructure, which have been identified as a major growth driver for the economy, slowed in implementation due to election-related delays. Nevertheless, low inflation, rising employment levels and rising recurrent fiscal spending are still boosting private investment and household consumption to close to their three-year high.

Knight Frank Thailand Research indicates that, in the second quarter, one new office building was completed outside the CBD. As a result, total supply in Bangkok increased by 46,000 square metres, to a total of 5,028,419sqm.

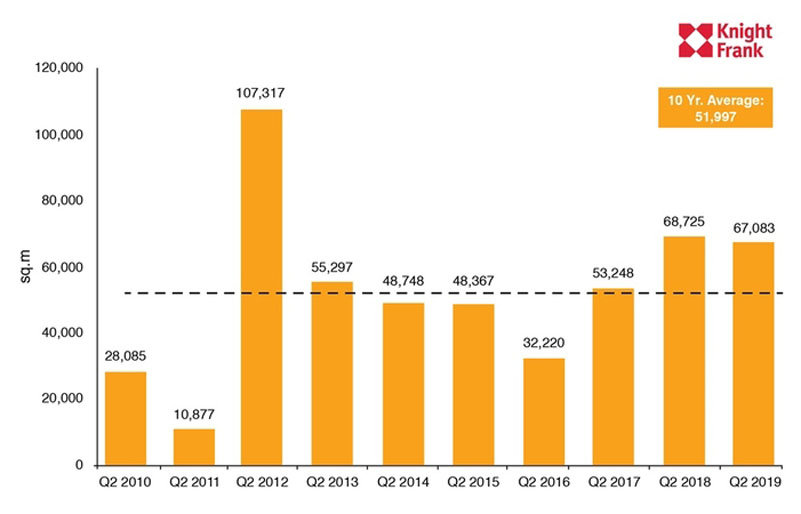

Despite slightly subdued occupier activity at the start of the year, market activity picked up considerably in the second quarter, as take-up increased to 67,083sqm from 37,974. A significant portion of the quarterly take-up occurred at the newly completed building, indicating tenants’ preferences for new supply. Although the take up is marginally lower Y-o-Y, it is still above the 10-year average of 51,997sqm.

Net absorption was positive at 5,910sqm in this quarter, increasing total occupied space to 4,575,121sqm. Despite the quarterly increase, total occupied space is still down Y-o-Y. Over the past 12 months, total supply increased by 30,190sqm, but total occupied space declined by 22,794. This suggests that annual demand was lower than supply.

Given the economic slowdown and lack of prime properties added to the CBD in the past year, current and potential tenants could be adopting a wait-and-see approach on any office relocation or expansion plans that they may have.

Overall market occupancy rate dropped to 91 per cent from 91.7 in Q2. Despite the slight decline, the market occupancy rate has remained relatively consistent. The rate has been within a healthy range of 91 per cent to 93 over the past five years, signalling a high level of stability in the market. CBD occupancy rates declined for three of the four areas sampled.

Only the Asok-Phrom Phong area, which also has the highest occupancy rate at 96.8 per cent, experienced no change in this quarter.

Outside the CBD, Asok-Petchburi has the highest occupancy rate at 93.8 per cent, despite having declined by 0.5 per cent Q-o-Q. The area maintains a high occupancy rate as a result of its close proximity to the CBD.

However, the company has maintained the expectation that demand will pick up throughout the rest of the year as a result of greater post-election political stability, albeit at a subdued level due to the current economic uncertainty and cautious outlook.

The office market response to the supply entering in the second half will be a key indicator of demand over the next few years. Given projections that supply will increase by 4.3 per cent annually from 2019 to 2023, occupancy rates will drop if demand lags behind supply.

If asking rents rise, it may occur at a slower pace as tenant bargaining power grows with increasing options of high-quality office space.

Source: https://www.nationthailand.com/property/30375429