Bangkok office market stays in flux

Bangkok office market stays in flux

Sector copes with changing demands

The Bangkok office market in 2026 is expected to remain highly competitive but more selective, as limited new supply, rising Grade A demand and ESG-driven relocations reshape leasing strategies, according to property consultancies.

Office landlords are being forced to reposition assets, invest in upgrades, and rethink tenant experience as occupiers increasingly favour premium, sustainable buildings over older, inefficient stock.

Aukit Pronpattanapairoj, head of office leasing at Cushman & Wakefield Thailand, said competition will remain intense in 2026, though supply-side pressure is easing compared with the past 2-3 years.

“Fewer new buildings are entering the market, while several recently completed offices have already achieved relatively high occupancy levels, reducing the oversupply stress that was seen earlier,” he said.

With limited additions, office rents have begun to edge up as vacancy rates declined in 2025, although overall demand growth remains gradual rather than accelerating sharply.

Mr Aukit said long-term market direction still needs close monitoring, as tenant expansion remains cautious amid economic uncertainty and corporate cost controls.

CBD-LED PIPELINE

CBD-LED PIPELINE

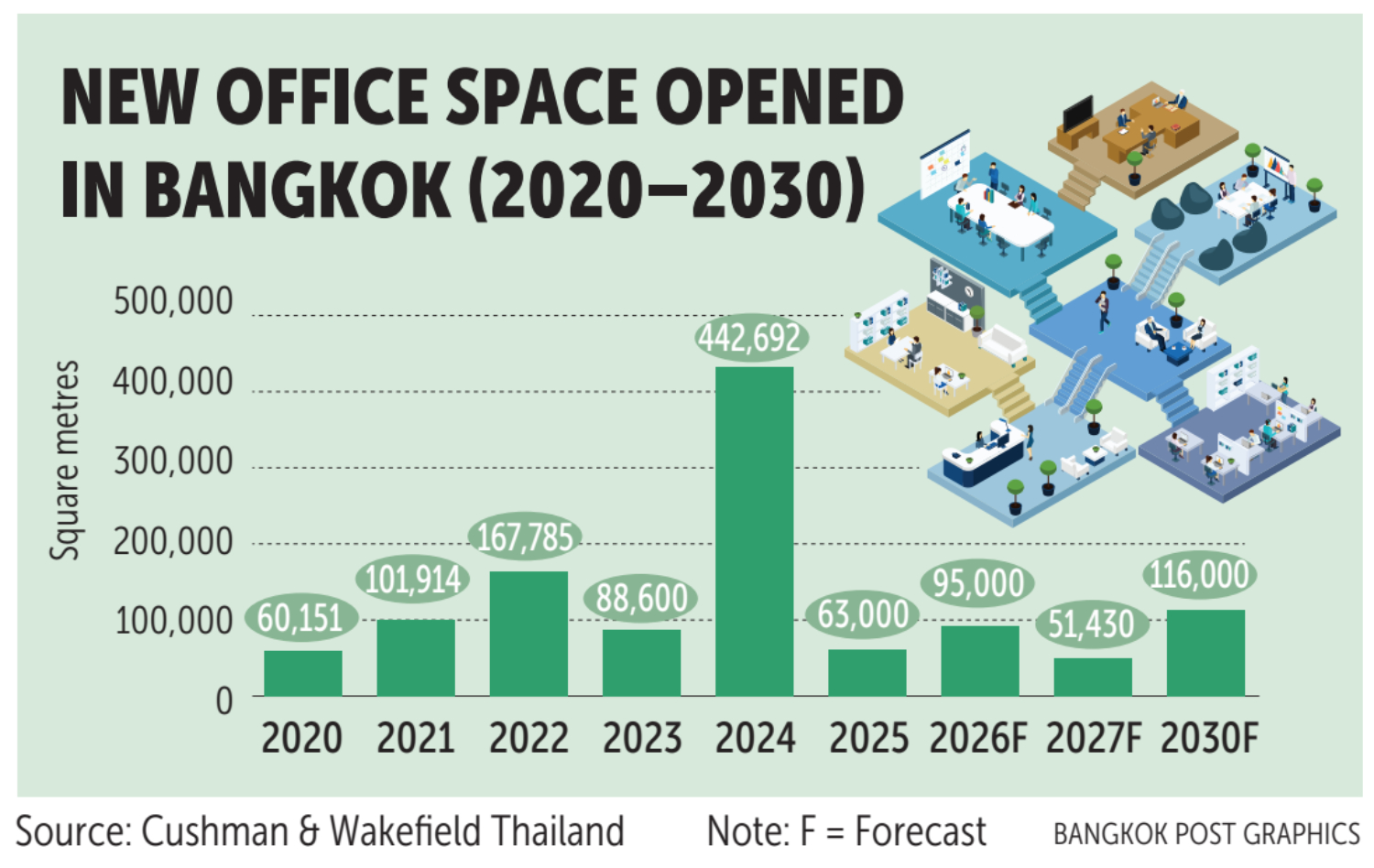

According to Cushman, Bangkok saw only two new office buildings open in 2025, adding a combined 101,000 square metres of leasable space, down 84% from 615,000 sq m delivered across 12 buildings in 2024.

A notable structural shift has been in the concentration of new supply within the central business district (CBD), where almost all recently completed projects are Grade A offices.

As a result, total Grade A office space in the CBD has increased to 2.53 million sq m, while Bangkok’s total office stock stood at about 8.99 million sq m at the end of 2025.

The CBD pipeline remains active, with further supply expected despite the broader slowdown, Mr Aukit added.

Between 2026 and 2030, Bangkok is projected to see about 591,800 sq m of new office space, of which roughly 262,400 sq m, or 44.3%, will be located in CBD areas.

FLIGHT TO QUALITY

Demand for high-quality offices has remained resilient, driven by new market entrants and tenants relocating or expanding within Grade A buildings.

This has pushed down overall Grade A vacancy rates to an estimated 23.8% in the fourth quarter of 2025, from 26% previously.

Average Grade A rents rose to 943 baht per sq m per month in the fourth quarter, up from 937 baht in the previous quarter, Cushman data showed.

While rents were slightly lower year-on-year, Mr Aukit said upward momentum is returning as new Grade A buildings achieve strong take-up without aggressive pricing incentives.

“2026 will remain competitive but less pressured, as limited new supply supports rental growth and continued vacancy reduction,” he said. “Tenant demand is increasingly driven by relocations from older offices to newer, environmentally certified buildings with modern amenities.”

These features have become critical requirements for multinational firms, particularly environmental, social and governance (ESG) compliance, energy efficiency, and employee wellbeing standards.

Krit Pimhataivoot, country head and head of capital markets at JLL Thailand, said that Bangkok’s office oversupply has accelerated a long-running “flight-to-quality” trend, which was first observed in 2016 and has intensified significantly following the pandemic.

“Corporate occupiers are now consolidating footprints and relocating to premium buildings, reshaping workplace strategies and leasing decisions,” he said.

“Outdated offices struggle due to inflexible layouts, weak ESG credentials and poor tenant experience, rather than rental pricing alone.”

CERTIFICATION GAP WIDENS

As of 2025, around 3.3 million sq m, or 30% of Bangkok’s office stock, has obtained building certification.

More than 90% of new supply since 2019 is ESG-compliant, with all upcoming projects until 2030 targeting LEED certification, placing older buildings at a clear disadvantage.

JLL said landlords should prioritise LEED Gold standards, WELL certification, and smart building systems covering energy, air quality and automation.

Cosmetic upgrades alone are insufficient, with meaningful infrastructure investment required to remain competitive.

BEYOND GREEN BUILDINGS

“Beyond physical retrofits, landlords are also focusing on social and governance initiatives, including wellness programmes and community activities, to enhance tenant engagement,” Mr Krit said.

ESG-certified buildings may not automatically command higher rents, but they help to preserve occupancy and pricing power, he added.

Some retrofitted CBD assets have maintained rents close to pre-pandemic levels while attracting tenants relocating from non-prime buildings.

JLL estimates that ESG-compliant offices can achieve rental premiums of about 14% above prime market averages.

UPGRADES CREATE UPSIDE

Roongrat Veeraparkkaroon, managing director of CBRE Thailand, said Bangkok’s office market remained active in 2025, with tenants benefiting from peak supply and favourable negotiating conditions.

“Many occupiers relocated to newer buildings as the flight-to-quality trend continued,” she said.

“Occupancy in top-tier Grade A+ offices has risen, which has allowed landlords to increase asking rents and widen performance gaps between prime and secondary assets.”

She said that a large number of landlords have accelerated asset enhancement plans as a result of weak overall conditions.

Once renovations are completed, older buildings will offer tenants more options when considering relocations or lease renewals.

“With very limited new office supply expected over the next four years, well-renovated buildings in established locations will present compelling relocation opportunities,” Ms Roongrat said.

She added that landlords who fail to adapt risk falling further behind in a market increasingly defined by quality, sustainability, and tenant experience, rather than sheer scale.

Source: https://www.bangkokpost.com/property/3189210/bangkok-office-market-stays-in-flux

Google Translation:

ตลาดอาคารสำนักงานในกรุงเทพฯ ยังคงผันผวน

ภาคส่วนนี้กำลังรับมือกับความต้องการที่เปลี่ยนแปลงไป

บริษัทที่ปรึกษาด้านอสังหาริมทรัพย์คาดการณ์ว่า ตลาดอาคารสำนักงานในกรุงเทพฯ ในปี 2026 จะยังคงมีการแข่งขันสูง แต่จะมีความเลือกสรรมากขึ้น เนื่องจากอุปทานใหม่มีจำกัด ความต้องการอาคารเกรด A ที่เพิ่มขึ้น และการย้ายที่ตั้งที่ขับเคลื่อนด้วย ESG กำลังปรับเปลี่ยนกลยุทธ์การเช่า

เจ้าของอาคารสำนักงานถูกบังคับให้ปรับเปลี่ยนสินทรัพย์ ลงทุนในการปรับปรุง และคิดใหม่เกี่ยวกับประสบการณ์ของผู้เช่า เนื่องจากผู้เช่าหันมานิยมอาคารระดับพรีเมียมและยั่งยืนมากกว่าอาคารเก่าที่ไม่มีประสิทธิภาพ

อยุกิตต์ พรปัตตานาไพโรจน์ หัวหน้าฝ่ายเช่าพื้นที่สำนักงานของ Cushman & Wakefield ประเทศไทย กล่าวว่า การแข่งขันจะยังคงรุนแรงในปี 2026 แม้ว่าแรงกดดันด้านอุปทานจะลดลงเมื่อเทียบกับ 2-3 ปีที่ผ่านมา

“อาคารใหม่เข้าสู่ตลาดน้อยลง ในขณะที่อาคารสำนักงานที่สร้างเสร็จใหม่หลายแห่งมีอัตราการเข้าใช้พื้นที่ค่อนข้างสูงแล้ว ซึ่งช่วยลดความเครียดจากอุปทานล้นตลาดที่เคยเห็นมาก่อน” เขากล่าว

ด้วยจำนวนอาคารสำนักงานใหม่ที่เพิ่มขึ้นอย่างจำกัด ค่าเช่าสำนักงานจึงเริ่มปรับตัวสูงขึ้นเล็กน้อย เนื่องจากอัตราการว่างงานลดลงในปี 2025 แม้ว่าการเติบโตของความต้องการโดยรวมยังคงค่อยเป็นค่อยไปมากกว่าที่จะเร่งตัวขึ้นอย่างรวดเร็ว

นายอุ๊กกิตกล่าวว่า ทิศทางตลาดในระยะยาวนั้นยังคงต้องติดตามอย่างใกล้ชิด เนื่องจากผู้เช่ายังคงขยายพื้นที่อย่างระมัดระวังท่ามกลางความไม่แน่นอนทางเศรษฐกิจและการควบคุมต้นทุนของบริษัท

ตลาดสำนักงานกรุงเทพฯ ยังคงผันผวน

โครงการในเขตศูนย์กลางธุรกิจ (CBD) เป็นศูนย์กลาง

จากข้อมูลของ Cushman กรุงเทพฯ มีอาคารสำนักงานใหม่เปิดให้บริการเพียง 2 แห่งในปี 2025 เพิ่มพื้นที่ให้เช่ารวม 101,000 ตารางเมตร ลดลง 84% จาก 615,000 ตารางเมตรใน 12 อาคารในปี 2024

การเปลี่ยนแปลงโครงสร้างที่เห็นได้ชัดคือการกระจุกตัวของอุปทานใหม่ในเขตศูนย์กลางธุรกิจ (CBD) ซึ่งโครงการที่สร้างเสร็จใหม่เกือบทั้งหมดเป็นอาคารสำนักงานเกรด A

ส่งผลให้พื้นที่สำนักงานเกรด A ในย่านศูนย์กลางธุรกิจ (CBD) เพิ่มขึ้นเป็น 2.53 ล้านตารางเมตร ขณะที่พื้นที่สำนักงานรวมของกรุงเทพฯ อยู่ที่ประมาณ 8.99 ล้านตารางเมตร ณ สิ้นปี 2568

นายอุ๊กกิตกล่าวเพิ่มเติมว่า โครงการก่อสร้างในย่าน CBD ยังคงดำเนินต่อไปอย่างต่อเนื่อง และคาดว่าจะมีอุปทานเพิ่มขึ้นอีก แม้ว่าเศรษฐกิจโดยรวมจะชะลอตัวลงก็ตาม

ระหว่างปี 2569 ถึง 2563 คาดว่ากรุงเทพฯ จะมีพื้นที่สำนักงานใหม่เพิ่มขึ้นประมาณ 591,800 ตารางเมตร โดยประมาณ 262,400 ตารางเมตร หรือ 44.3% จะอยู่ในย่าน CBD

ความต้องการพื้นที่สำนักงานคุณภาพสูงยังคงแข็งแกร่ง โดยได้รับแรงหนุนจากผู้เข้ามาใหม่ในตลาด และผู้เช่าที่ย้ายหรือขยายธุรกิจภายในอาคารเกรด A

ส่งผลให้อัตราการว่างของพื้นที่สำนักงานเกรด A โดยรวมลดลงเหลือประมาณ 23.8% ในไตรมาสที่สี่ของปี 2568 จาก 26% ก่อนหน้านี้

ข้อมูลจาก Cushman แสดงให้เห็นว่า ค่าเช่าเฉลี่ยของอาคารเกรด A เพิ่มขึ้นเป็น 943 บาทต่อตารางเมตรต่อเดือนในไตรมาสที่สี่ จาก 937 บาทในไตรมาสก่อนหน้า

แม้ว่าค่าเช่าจะลดลงเล็กน้อยเมื่อเทียบกับปีก่อนหน้า แต่คุณอกิตกล่าวว่า โมเมนตัมขาขึ้นกำลังกลับมา เนื่องจากอาคารเกรด A ใหม่ได้รับความสนใจอย่างมากโดยไม่ต้องใช้กลยุทธ์การกำหนดราคาที่ดุดัน

“ปี 2026 จะยังคงมีการแข่งขันสูง แต่แรงกดดันจะลดลง เนื่องจากอุปทานใหม่มีจำกัด ซึ่งสนับสนุนการเติบโตของค่าเช่าและการลดลงของอัตราการว่างงานอย่างต่อเนื่อง” เขากล่าว “ความต้องการของผู้เช่าได้รับแรงผลักดันมากขึ้นจากการย้ายจากสำนักงานเก่าไปยังอาคารใหม่ที่ได้รับการรับรองด้านสิ่งแวดล้อม พร้อมสิ่งอำนวยความสะดวกที่ทันสมัย”

คุณสมบัติเหล่านี้กลายเป็นข้อกำหนดที่สำคัญสำหรับบริษัทข้ามชาติ โดยเฉพาะอย่างยิ่งการปฏิบัติตามข้อกำหนดด้านสิ่งแวดล้อม สังคม และธรรมาภิบาล (ESG) ประสิทธิภาพด้านพลังงาน และมาตรฐานความเป็นอยู่ที่ดีของพนักงาน

กฤษิต พิมหัตถ์วุฒิ หัวหน้าฝ่ายตลาดทุนและประธานเจ้าหน้าที่บริหาร เจแอลแอล ประเทศไทย กล่าวว่า อุปทานส่วนเกินของอาคารสำนักงานในกรุงเทพฯ ได้เร่งให้เกิดแนวโน้ม “การหนีไปสู่คุณภาพ” ที่เกิดขึ้นมานานแล้ว ซึ่งเริ่มสังเกตเห็นครั้งแรกในปี 2559 และทวีความรุนแรงขึ้นอย่างมากหลังจากการระบาดใหญ่

“ผู้เช่าพื้นที่สำนักงานกำลังรวมพื้นที่และย้ายไปยังอาคารระดับพรีเมียม ปรับเปลี่ยนกลยุทธ์สถานที่ทำงานและการตัดสินใจเช่า” เขากล่าว

“อาคารสำนักงานที่ล้าสมัยประสบปัญหาเนื่องจากรูปแบบที่ไม่ยืดหยุ่น คุณสมบัติ ESG ที่อ่อนแอ และประสบการณ์ของผู้เช่าที่ไม่ดี มากกว่าราคาค่าเช่าเพียงอย่างเดียว”

ช่องว่างด้านการรับรองกว้างขึ้น

ณ ปี 2568 อาคารสำนักงานประมาณ 3.3 ล้านตารางเมตร หรือ 30% ของพื้นที่สำนักงานในกรุงเทพฯ ได้รับการรับรองอาคารแล้ว

มากกว่า 90% ของอุปทานใหม่ตั้งแต่ปี 2562 เป็นไปตามมาตรฐาน ESG โดยโครงการที่จะเกิดขึ้นทั้งหมดจนถึงปี 2563 ตั้งเป้าหมายที่จะได้รับการรับรอง LEED ซึ่งทำให้อาคารเก่าเสียเปรียบอย่างชัดเจน

JLL กล่าวว่าเจ้าของอาคารควรให้ความสำคัญกับมาตรฐาน LEED Gold, การรับรอง WELL และระบบอาคารอัจฉริยะที่ครอบคลุมด้านพลังงาน คุณภาพอากาศ และระบบอัตโนมัติ

การปรับปรุงตกแต่งเพียงอย่างเดียวไม่เพียงพอ จำเป็นต้องมีการลงทุนด้านโครงสร้างพื้นฐานอย่างมีนัยสำคัญเพื่อให้สามารถแข่งขันได้

นอกเหนือจากอาคารสีเขียว

“นอกเหนือจากการปรับปรุงทางกายภาพแล้ว เจ้าของอาคารยังให้ความสำคัญกับโครงการริเริ่มด้านสังคมและการกำกับดูแล รวมถึงโปรแกรมด้านสุขภาพและกิจกรรมชุมชน เพื่อเพิ่มการมีส่วนร่วมของผู้เช่า” นายกฤตกล่าว

อาคารที่ได้รับการรับรอง ESG อาจไม่ได้ทำให้ค่าเช่าสูงขึ้นโดยอัตโนมัติ แต่ช่วยรักษาอัตราการเข้าอยู่อาศัยและอำนาจในการกำหนดราคา เขากล่าวเสริม

สินทรัพย์ CBD บางแห่งที่ได้รับการปรับปรุงใหม่สามารถรักษาค่าเช่าไว้ได้ใกล้เคียงกับระดับก่อนเกิดโรคระบาด ในขณะเดียวกันก็ดึงดูดผู้เช่าที่ย้ายมาจากอาคารที่ไม่ใช่ทำเลทอง

JLL ประมาณการว่าสำนักงานที่สอดคล้องกับ ESG สามารถบรรลุค่าเช่าที่สูงกว่าค่าเฉลี่ยของตลาดทำเลทองได้ประมาณ 14%

การปรับปรุงสร้างโอกาสที่ดีขึ้น

คุณรุ่งรัตน์ วีระปาร์คการูน กรรมการผู้จัดการ CBRE ประเทศไทย กล่าวว่า ตลาดอาคารสำนักงานในกรุงเทพฯ ยังคงคึกคักในปี 2025 โดยผู้เช่าได้รับประโยชน์จากอุปทานที่สูงสุดและเงื่อนไขการเจรจาต่อรองที่เอื้ออำนวย

“ผู้เช่าจำนวนมากย้ายไปอยู่ในอาคารใหม่กว่า เนื่องจากกระแสการย้ายไปอยู่ในอาคารคุณภาพสูงยังคงดำเนินต่อไป” เธอกล่าว

“อัตราการเข้าใช้พื้นที่ในอาคารสำนักงานเกรด A+ ระดับสูงเพิ่มขึ้น ซึ่งทำให้เจ้าของอาคารสามารถเพิ่มค่าเช่าและขยายช่องว่างประสิทธิภาพระหว่างสินทรัพย์ชั้นดีและสินทรัพย์รองได้”

เธอกล่าวว่า เจ้าของอาคารจำนวนมากได้เร่งแผนการปรับปรุงสินทรัพย์เนื่องจากสภาวะโดยรวมที่อ่อนแอ

เมื่อการปรับปรุงเสร็จสมบูรณ์ อาคารเก่าจะให้ทางเลือกแก่ผู้เช่ามากขึ้นเมื่อพิจารณาการย้ายที่ตั้งหรือการต่อสัญญาเช่า

“ด้วยอุปทานอาคารสำนักงานใหม่ที่คาดว่าจะจำกัดมากในช่วงสี่ปีข้างหน้า อาคารที่ได้รับการปรับปรุงอย่างดีในทำเลที่เป็นที่ยอมรับจะนำเสนอโอกาสในการย้ายที่ตั้งที่น่าสนใจ” คุณรุ่งรัตน์กล่าว

เธอกล่าวเสริมว่า เจ้าของที่ดินที่ไม่ปรับตัวมีความเสี่ยงที่จะล้าหลังไปอีกในตลาดที่นับวันยิ่งถูกกำหนดด้วยคุณภาพ ความยั่งยืน และประสบการณ์ของผู้เช่า มากกว่าขนาดที่ใหญ่โตเพียงอย่างเดียว